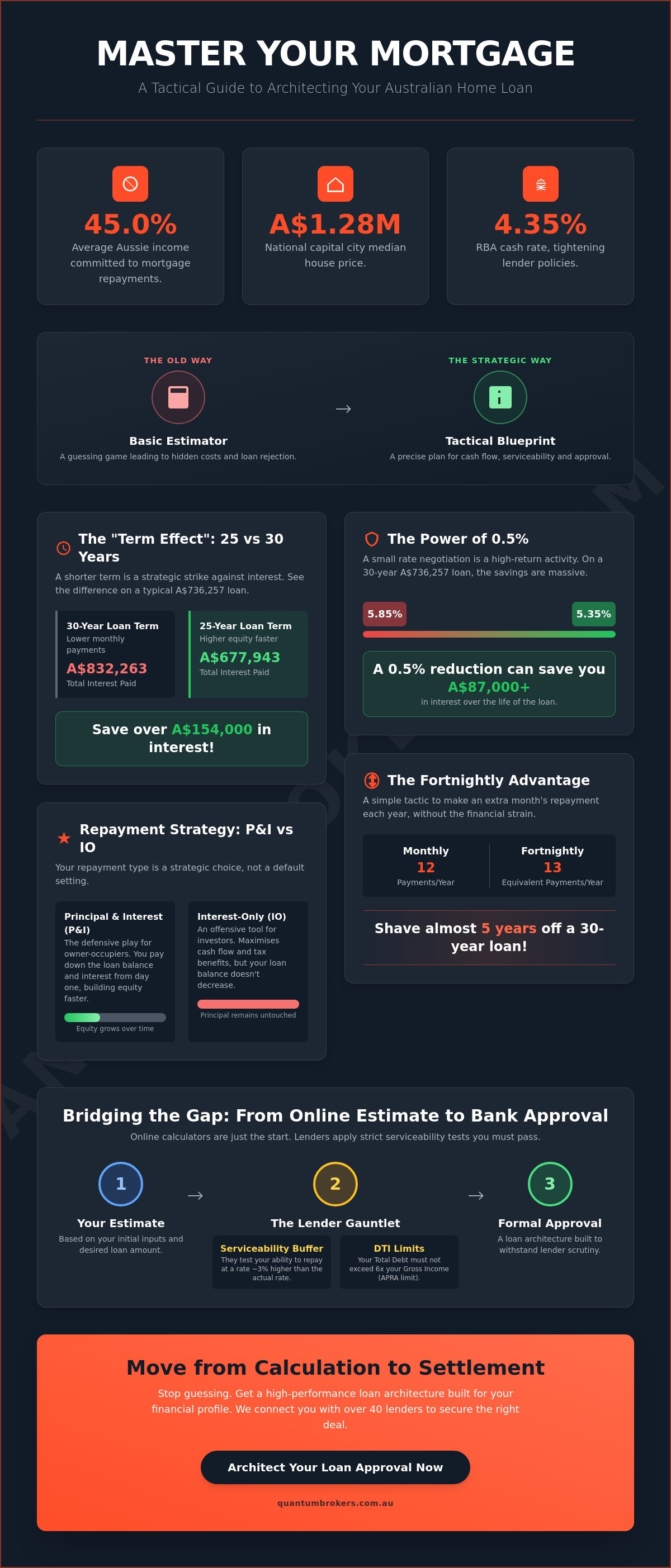

With Australians now committing an average of 45.0% of their income to mortgage repayments, a standard online tool isn't enough to secure your financial future. Stop treating your home loan like a guessing game. Most borrowers use a basic mortgage calculator to find a number they like, only to be blindsided by hidden costs or APRA's strict debt-to-income limits. You don't need a rough estimate. You need a blueprint. In a market where the national capital city median house price has climbed to A$1,287,476, guessing is a luxury you can't afford.

It's natural to feel anxious about serviceability when the RBA cash rate sits at 4.35% and banks are tightening their frameworks. This guide will show you how to master the variables of your next loan, moving you from basic estimation to a tactical approval strategy. We will examine how to account for shifting interest rates, the massive impact of extra repayments on your loan term, and the specific data required to architect a high-performance home loan with total confidence.

Key Takeaways

- Transform your mortgage calculator from a basic estimator into a tactical reconnaissance tool for precise cash flow forecasting in the 2026 market.

- Decipher the "Term Effect" to understand how choosing between 25 and 30-year loan structures dictates your long-term interest costs.

- Identify the hidden serviceability buffers Australian lenders apply so you can bridge the gap between an online estimate and a formal bank approval.

- Stress-test your strategy against future rate hikes and learn how tactical offset accounts can accelerate your path to total home ownership.

- Move from calculation to settlement by accessing a network of over 40 lenders to secure a loan architecture that fits your specific financial profile.

The Tactical Role of an Australian Mortgage Calculator in 2026

Most Australians treat a mortgage calculator like a digital toy. They plug in a dream house price, see a repayment figure they might be able to stomach, and hope for the best. That approach is a recipe for financial failure in 2026. You must treat this tool as a tactical reconnaissance instrument. With the RBA holding the official cash rate at 4.35% as of May 2026, every decimal point in your interest rate dictates your long-term wealth. Precise cash flow forecasting isn't optional; it's the foundation of your loan architecture.

A mortgage calculator serves as your first line of financial modelling. It allows you to move beyond simple interest math and into the territory of tactical loan structuring. While basic arithmetic tells you what you owe today, a strategic model accounts for the shifting market conditions and APRA's strict debt-to-income (DTI) limits. If your DTI ratio exceeds six times your gross income, you fall into a high-risk category that banks now limit to just 20% of their new lending. Accurate data entry is the only way to ensure your outputs are reliable. If you underestimate your living expenses or ignore your credit cards, your strategy will collapse before you reach the bank's assessment desk.

Why Estimates Are Your Financial Reconnaissance

Data defines your boundaries. Use a calculator to establish your maximum purchase price before you set foot in an open home. With the national capital city median house price sitting at A$1,287,476, you need to identify the "sweet spot" for your deposit size and Loan-to-Value Ratio (LVR). Aiming for an 80% LVR is the standard play to avoid Lenders Mortgage Insurance (LMI), but in 2026, many first home buyers are tactically using the Federal Government’s Home Guarantee Scheme to secure a property with just a 5% deposit. Use your reconnaissance data to set realistic expectations and avoid the heartbreak of being outbid on a property you can't actually service.

The Principal and Interest vs. Interest-Only Debate

Your repayment type is a strategic choice, not a default setting. Principal and Interest (P&I) repayments build equity faster by reducing the loan balance from day one. In contrast, Interest-Only (IO) structures are often used by investors to maximise tax deductibility and maintain cash flow for other assets. However, the long-term cost of IO is significantly higher because the principal remains untouched, leading to higher total interest over the life of the loan. Calculate the difference over a five-year window to see the impact. While P&I is the defensive play for owner-occupiers, IO can be a powerful offensive tool for portfolio growth if managed with precision.

Decoding the Variables: How Interest and Terms Impact Cash Flow

Every decimal point on your home loan is a lever. In May 2026, the RBA cash rate sits at 4.35%, pushing variable rates for many borrowers into the high 5% range. If you aren't modelling these variables, you're bleeding capital. A standard mortgage calculator reveals the "Term Effect" in stark detail. A 30-year term is the default choice for most because it minimises monthly cash flow pressure. However, a 25-year term is a strategic strike against interest. The interest you pay is "dead money". It is bank profit that adds nothing to your equity. Shortening your term by five years can save you six figures in interest over the life of a typical A$736,257 loan.

The True Cost of a 0.5% Rate Variance

Negotiating a 0.5% reduction is a high-ROI activity. On a large loan, that small variance translates to massive savings over time. This is why this guide to mortgages is essential reading for architecting a better deal. Using a mortgage calculator to model a 0.5% reduction reveals how much you can truly save. Look past the headline rate and scrutinise the comparison rate. It includes mandatory fees and charges, providing the true cost of the debt. If your current lender won't move, you should consider a strategic refinance to unlock better terms.

Fortnightly Repayments: The Hidden Strategy

Switching from monthly to fortnightly cycles is a simple but powerful tactic. By paying half your monthly amount every two weeks, you make 26 half-payments a year. This equals 13 full monthly payments instead of 12. This extra month of repayments attacks the principal balance directly. It can shave years off your loan term without requiring a radical lifestyle change. Aligning these payments with your income cycle creates a seamless, high-performance repayment structure. It ensures your money works for you the moment it hits your account.

The Gap Between Online Estimates and Lender Approval

A "green light" on a basic mortgage calculator is often a mirage. It doesn't account for the opaque credit policies that govern Australian lending in 2026. While you might see a repayment you can afford, the bank sees a risk profile they might not want. This gap exists because lenders don't calculate your serviceability based on the advertised rate. They use a serviceability buffer, typically 3% above the current product rate, to stress-test your finances against future shocks. If you are looking at a variable rate of 5.89%, the bank is actually assessing your ability to pay at 8.89%. This is a massive hurdle that most online tools ignore.

Your existing liabilities are "capacity killers" in the eyes of a credit assessor. HECS/HELP debts, car loans, and credit card limits (not just balances) are factored in with brutal efficiency. Even if you don't use your A$10,000 credit card limit, the bank treats it as a potential debt that could be maxed out tomorrow. This reduces your borrowing power by thousands. Using Moneysmart's mortgage calculator provides a solid baseline for repayments, but it cannot mirror the proprietary algorithms banks use to judge your lifestyle. Under APRA's 2026 rules, if your total debt exceeds six times your gross income, your application enters a high-scrutiny zone where only 20% of new lending is permitted.

Lender Serviceability vs. Your Personal Budget

Banks use the Household Expenditure Measure (HEM) to benchmark your spending. If your actual expenses are lower than the HEM benchmark for your demographic, the bank will likely use the higher HEM figure anyway. They are "stress testing" your survival, not your comfort. To improve your paper serviceability, you must clean up your bank statements three to six months before applying. Cancel unused subscriptions and close down high-limit credit cards. These are tactical moves that turn a "maybe" into a "yes" during the assessment phase.

The Self-Employed and NDIS Income Challenge

Standard calculators fail business owners because they don't understand the nuance of "add-backs." We look for depreciation, one-off expenses, and additional superannuation contributions that can be added back to your net profit to boost your borrowing power. Similarly, NDIS property finance requires a specialist approach. Lenders treat NDIS rental income differently than standard residential rent. Some will only recognise a portion of the projected high-yield income, while others have specific frameworks for Specialist Disability Accommodation (SDA). Architecting these complex income streams requires a master of the system, not just a simple web tool.

Stress-Testing Your Strategy: Preparing for Rate Fluctuations

Hoping for interest rate stability is a losing strategy. In a market where the RBA cash rate sits at 4.35%, you must architect a loan that survives volatility. Don't just calculate what you owe today. Use a mortgage calculator to model your repayments at 2% above current market rates. If that figure breaks your monthly budget, your current financial structure is high-risk. This exercise isn't about pessimism; it's about tactical reconnaissance. By identifying your "breaking point" now, you can deploy defensive measures like redraw facilities or a fixed-rate split before the market shifts against you.

A fixed vs. variable split is a powerful risk mitigation tool. It allows you to hedge your bets, locking in a portion of your debt at 2026's competitive fixed rates while keeping the remainder variable to access features like offset accounts. This hybrid architecture provides a ceiling on your most significant expense while maintaining the liquidity you need to stay agile. If you want to see how these levers change your bottom line, you should secure your financial future with a custom loan structure designed for the long haul.

Building Your Interest Rate Buffer

Paying only the minimum requirement is a defensive failure. Strategic borrowers treat the difference between their actual rate and their "stress-test rate" as a mandatory contribution. If you model a worst-case scenario using a mortgage calculator, you can see exactly how much extra cash you need to set aside to remain bulletproof. This extra capital should be directed into an offset account or redraw facility. This creates a dual-purpose shield: it reduces the interest you pay today and provides a liquidity reserve for tomorrow. It's the difference between being a victim of the market and being a master of it.

Offset Accounts: The Strategic Equity Deployment

An offset account is the ultimate weapon against "dead money." Consider the impact of holding A$50,000 in a 100% offset account against a standard home loan. At a 6% interest rate, that capital saves you A$3,000 in interest annually. Because this is interest saved rather than income earned, it is effectively a tax-free return on your money. While additional repayments into the loan balance are permanent, offset funds remain accessible for future investments or emergencies. We prioritise this level of flexibility for our clients because it keeps your capital working for you without locking it away. Compare this against a standard savings account, and the strategic advantage is clear.

From Calculation to Settlement: Architecting Your Loan Approval

A mortgage calculator provides the coordinates, but it doesn't fly the plane. Moving from a digital estimate to a signed contract requires a specialist who knows the terrain. Banks are bound by their own narrow appetites. If you don't fit their specific box, they'll reject you without a second thought. We operate differently. As your strategic advocate, we bridge the gap between initial data and final settlement. We don't just find a loan; we architect a solution that survives the scrutiny of credit assessors across 40+ different lenders. This is the difference between a generic "no" and a tactical approval.

The path from calculation to settlement is a multi-stage operation. It begins with your initial modelling, but it must quickly transition into a formal strategy. We take your raw data and stress-test it against the proprietary policies of dozens of Australian institutions. This process identifies the lender most likely to appreciate your specific financial profile. Whether you are looking for first home buyer loans or complex investment loans, the goal is to move you toward pre-approval with total speed. In a market where the national median dwelling value is A$922,838, hesitation costs money. We eliminate that delay by positioning your application for an immediate "yes."

Unlocking Complex Lending Scenarios

Standard lenders often struggle with non-traditional income. If you are navigating the complexities of NDIS property finance, you need a partner who understands these specialised frameworks. Many big banks see the high-yield nature of Specialist Disability Accommodation (SDA) as a risk they aren't equipped to handle. We see it as a strategic asset. The same applies to self-employed borrowers. While a bank might focus on your tax returns from two years ago, we use add-backs and current profit projections to secure approvals where others have failed. We turn the rigid "no" of a traditional institution into a tactical "yes" through superior loan structuring.

Secure Your Tactical Advantage Today

Speed is a currency in the 2026 property market. Waiting weeks for a bank to process a simple inquiry is a strategic failure. You need an accurate assessment of your borrowing power before you lose your preferred property to a faster bidder. Our 24-hour borrowing power assessment moves you from the "what if" of a mortgage calculator to the "what's next" of a formal pre-approval. Precision and pace are non-negotiable. Don't leave your settlement to chance. It's time to unlock your financing options with a Quantum Brokers specialist and take command of your financial future.

Command Your Financial Future: From Blueprint to Settlement

Your home loan isn't a passive debt; it's a structural foundation that requires precise engineering. While a basic mortgage calculator identifies your starting point, it cannot navigate the shifting serviceability buffers and APRA regulations defining the 2026 market. Success requires moving beyond simple estimation to a strategy that accounts for interest rate stress-tests and complex income variables. You now have the framework to transform raw data into a tactical advantage.

Stop guessing and start architecting. Whether you are navigating the complexities of NDIS property finance or require a specialist approach for self-employed income, we provide the technical mastery to secure your approval. With access to 40+ Australian lenders and our 24-hour borrowing power assessment, we turn market obstacles into strategic victories. Architect your loan approval with Quantum Brokers and take the first decisive step toward your next property milestone today. Your future home is waiting for its architect.

Frequently Asked Questions

How accurate are online mortgage calculators for Australian loans?

Online calculators provide a mathematical baseline but lack the nuance of lender-specific credit policy. Most tools assume you meet perfect criteria without accounting for your specific risk profile. In reality, your actual repayment depends on the lender's internal assessment and current market margins. Use a mortgage calculator for initial reconnaissance, but rely on a broker to architect the final approved figure based on 2026 lending frameworks.

Does using a mortgage calculator affect my credit score?

Using an online calculator has zero impact on your credit score. It is a private modelling tool that doesn't require a credit check or personal identification. You can run as many scenarios as you need to stress-test your strategy without leaving a footprint. A hard enquiry only occurs when you submit a formal application to a lender, which is why pre-calculation is a safe defensive move.

What is the difference between an interest rate and a comparison rate?

The interest rate is the percentage charged on your loan balance, while the comparison rate represents the true cost of the debt. The comparison rate is a legal requirement in Australia designed to reveal hidden costs. It factors in the base rate plus mandatory fees, such as the average annual package fee of A$374. Always use the comparison rate to model the real financial impact on your cash flow.

Can I use a mortgage calculator for an NDIS investment property?

You can use a mortgage calculator for NDIS property finance, but standard tools won't capture the high-yield reality of Specialist Disability Accommodation. These investments require specific modelling for government-backed income streams. A basic tool might show you the debt cost, but it fails to architect the complex serviceability required for NDIS-specific lending structures. Specialist input is essential to bridge this gap.

How do extra repayments change my loan calculation?

Extra repayments accelerate your equity growth by attacking the principal balance directly. This reduces the amount of interest calculated on your loan every month, creating a compounding saving effect. Even small, consistent additions can shave years off a standard 30-year term. Model these tactical injections to see how they transform your total interest bill and shorten your path to total home ownership.

Why is my bank borrowing limit different from the calculator result?

Banks use the Household Expenditure Measure (HEM) and a 3% serviceability buffer that most calculators ignore. While a calculator might show you can afford a loan at 5.89%, a bank will test your survival at 8.89%. They also scrutinise your debt-to-income ratio. If your total debt exceeds six times your income, APRA's 2026 rules will likely restrict your borrowing capacity regardless of what a web tool suggests.

Should I calculate my mortgage based on a 25 or 30-year term?

Choose a 30-year term if your priority is monthly cash flow flexibility. Select a 25-year term if your goal is to minimise the "dead money" paid to the bank in interest. A 30-year loan has lower monthly commitments but costs significantly more over the life of the debt. Many strategic borrowers take a 30-year term for safety but make repayments as if it were a 25-year loan to build equity faster.

What fees should I include in my home loan calculation?

Include the average mortgage application fee of A$487 and conveyancing costs ranging from A$1,200 to A$2,400 in your total calculation. You must also account for annual package fees and potential stamp duty. These upfront and ongoing costs are the friction of property finance. Failing to architect these into your initial budget leads to a capital shortfall at the point of settlement.