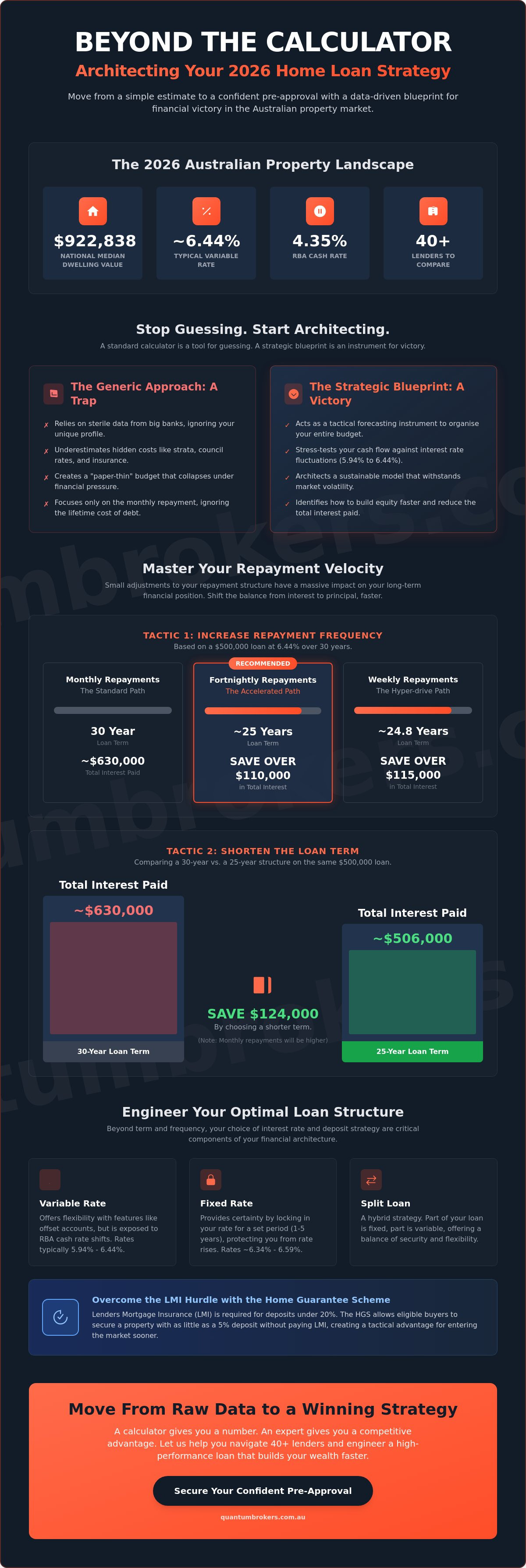

A standard mortgage repayment calculator is not a financial strategy; it is a diagnostic starting point that most buyers use incorrectly. With the national median dwelling value sitting at $922,838 and variable rates hovering around 6.44 per cent, guessing your monthly commitment is a high-risk gamble. You need more than a generic estimate. You need a blueprint that accounts for the 4.35 per cent RBA cash rate and the tactical nuances of the 2026 property market.

We understand the frustration of watching hidden costs like Lenders Mortgage Insurance erode your deposit while you struggle to compare 40+ lenders. It is time to stop reacting to the market and start architecting your position. This guide will show you how to master your cash flow and unlock the tactical data required to secure a high-performance home loan. We will break down the mechanics of interest reduction and provide the clarity you need to move from a simple calculation to a confident pre-approval.

Key Takeaways

- Use a mortgage repayment calculator as a tactical forecasting instrument to organise your household budget before approaching lenders.

- Master repayment velocity by identifying how weekly or fortnightly schedules aggressively reduce interest and build equity.

- Unlock the strategic data behind loan terms to see exactly how a 25-year versus 30-year structure impacts your long-term financial victory.

- Model repayments for specialised scenarios, including NDIS property finance and irregular self-employed income, to ensure total lending viability.

- Secure a high-performance loan structure by moving beyond raw data and leveraging expert insights to navigate 40+ Australian lenders.

Architecting Your Future: Why the Mortgage Repayment Calculator is Your First Strategic Move

Property finance in 2026 is no longer a game of simple arithmetic; it is a high-stakes design challenge. To succeed, you must view a mortgage repayment calculator as a tactical forecasting instrument rather than a passive estimation tool. While most borrowers use these tools to satisfy a vague curiosity, a strategic borrower uses them to organise their entire household budget before ever stepping foot in a bank. You are not just looking for a number. You are architecting a sustainable cash flow model that survives market volatility.

The generic tools provided by the "Big Four" banks often fall short. They are designed for the average consumer, offering sterile data that ignores the complexities of your specific financial profile. At Quantum Brokers, we advocate for a broker-led approach to data. This means using current 2026 interest rate projections, where owner-occupier variable rates sit between 5.94 per cent and 6.44 per cent, to stress-test your strategy. If your plan only works at the lower end of that spectrum, your architecture is flawed. You need a structure that holds firm even when the RBA cash rate shifts.

Forecasting vs. Guessing: The Data-Driven Advantage

Precise data entry is the non-negotiable foundation of a successful loan application. If your inputs are flawed, your results are dangerous. You should utilise our comprehensive home mortgage guide to identify the exact figures required for an accurate simulation. Many Australians sabotage their own strategy by underestimating hidden costs like council rates, strata fees, and building insurance. These are not optional extras; they are structural components of your monthly cash flow. Ignoring them creates a "paper-thin" budget that collapses under the first sign of financial pressure.

Beyond the Monthly Figure: Total Interest Awareness

A tactical borrower looks past the immediate monthly commitment to understand the lifetime cost of the debt. This is where you find your victory. Understanding What is a mortgage calculator? allows you to manipulate variables like principal and term to see the long-term impact. Small adjustments to the interest rate lever can save you six figures over a 30-year period. Loan amortisation is the systematic reduction of debt over time. By visualising this process, you can identify exactly when your equity begins to outpace your interest, allowing you to secure a high-performance loan that builds wealth faster than a standard bank-issued product.

Decoding the Mechanics: How Interest Rates and Terms Dictate Your Repayment Velocity

Think of your mortgage repayment as a machine with two primary gears: principal and interest. Every time you use a mortgage repayment calculator, you are essentially testing how these gears interact over the long term. The principal is the raw debt you owe. The interest is the fee for the privilege of the debt. In the early years of a standard 30-year term, the interest component dominates the structure. To achieve true financial victory, you must shift the balance toward principal as quickly as possible. This is what we call repayment velocity.

Lenders Mortgage Insurance (LMI) is often the "hidden" weight in this machine. If your deposit is less than 20 per cent, you will likely face this one-off cost, which can be capitalised into the loan. While this increases your monthly commitment, it is a tactical trade-off for entering the market sooner. Strategic borrowers in 2026 are already leveraging the Home Guarantee Scheme to secure properties with a 5 per cent deposit without the LMI burden, effectively bypassing this obstacle entirely. Understanding these nuances is why consulting a specialist is the fastest way to move from raw data to a functional finance strategy.

The Interest Rate Lever: Variable, Fixed, and Split Strategies

Your choice of interest rate dictates your blueprint's stability. Variable rates offer flexibility and features like offset accounts, but they expose you to the RBA's 4.35 per cent cash rate fluctuations. Fixed rates, currently ranging from 6.34 per cent for one year to 6.59 per cent for three years at major banks, provide a ceiling for your expenses. A split loan strategy is often the superior architectural choice. It allows you to hedge your position by fixing a portion for certainty while leaving the rest variable to take advantage of offset velocity. You must model a "buffer" of at least 2 to 3 per cent above current rates to ensure your cash flow survives any future market shifts.

The 30-Year Blueprint: Why Term Length Matters

Term length is the most significant multiplier of total cost. A 30-year term is the industry standard because it keeps monthly repayments manageable. However, it is also the most expensive way to borrow. By architecting a 25-year term instead, you increase your monthly commitment but slash the total interest paid over the life of the loan. For investment properties, a longer term might be a strategic move to preserve cash flow and maximise rental yields, which averaged 4.69 per cent nationally in early 2026. The goal is to match the term to your specific objective: aggressive equity growth for your home or cash flow optimisation for your portfolio.

Tactical Optimisation: Reducing Interest and Accelerating Equity Growth

Viewing your debt as a static obligation is a strategic failure. High-performance borrowers treat their home loan as a dynamic structure that can be optimised for speed. This is the essence of repayment velocity. While a mortgage repayment calculator provides the baseline, tactical optimisation involves manipulating payment frequency and liquidity to crush interest costs. You aren't just paying a bill. You are engineering a path to early financial freedom by outmanoeuvring the bank's standard interest calculations.

Extra repayments and redraw facilities are your primary tools for architecting this freedom. Every dollar paid above the minimum requirement attacks the principal directly, bypassing the interest-heavy front end of the loan. This is not about making massive sacrifices. It is about consistent, tactical injections of capital that shorten your debt horizon. By maintaining a redraw facility, you keep this capital accessible, providing a safety net while your equity grows at an accelerated rate.

The Fortnightly Advantage: Engineering 13 Months of Progress

The mathematics of payment frequency is one of the most underutilised levers in Australian finance. By switching from monthly to fortnightly repayments, you effectively make 26 half-payments per year. This total equals 13 full monthly payments rather than 12. This simple structural change shaves years off a 30-year term without requiring a change in your standard of living. Early principal reduction triggers a compounding effect that systematically erodes the interest-bearing balance of your debt. You are essentially tricking the system to work in your favour.

Offset Accounts: The Strategic Architect’s Favourite Tool

An offset account is the ultimate tactical edge for maintaining liquidity while reducing interest. Unlike a basic savings account, where interest earned is taxed, an offset account reduces the balance upon which your mortgage interest is calculated. You can use our refinance savings calculator australia to model how your specific cash reserves can slash your lifetime interest bill. This structure allows you to keep your funds liquid for future investments or emergencies while simultaneously neutralising the cost of your debt. It is the difference between letting your money sit idle and putting it to work in the foundation of your property strategy.

Navigating Complexity: Repayment Strategies for Self-Employed and NDIS Investors

Standard financial institutions often treat irregular income as a structural flaw. At Quantum Brokers, we view it as a design variable to be mastered. If you are self-employed or an NDIS investor, a generic mortgage repayment calculator often feels like a blunt instrument that fails to account for your specific cash flow reality. You don't need a tool that assumes a static 9-to-5 PAYG salary. You need a strategy that bridges the gap between complex income streams and the rigid frameworks of Australian lending.

We act as the "Expert Fixer" for borrowers who have been told "no" by the Big Four banks. Whether you are navigating seasonal business fluctuations or the high-yield nuances of NDIS property finance, your repayment blueprint must be built on technical mastery rather than guesswork. Victory in these scenarios requires moving beyond raw data to architect a loan structure that reflects your true borrowing power.

The Self-Employed Tactical Briefing

Lenders typically require two years of personal and business tax returns to verify serviceability. However, we navigate alternative pathways for those with only six months of ABN history through low-doc and non-bank lending frameworks. When using a mortgage repayment calculator, self-employed borrowers should focus on their net profit after expenses rather than gross turnover to ensure a realistic commitment. We recommend architecting a "repayment buffer" equivalent to three months of commitments to neutralise the risk of seasonal cash flow dips, ensuring your property strategy remains resilient year-round.

NDIS Property Cash Flow: A Different Breed of Calculation

Specialist Disability Accommodation (SDA) property investments are high-performance assets that require a unique serviceability model. Unlike standard residential investments, NDIS properties often feature government-backed rental yields ranging from 8 to 12 per cent. This significantly alters your repayment capacity. You must factor in a 20 per cent deposit requirement, which is the standard for most specialist NDIS lenders in 2026. Because these loans are structured around high-yield rental income and long-term tenancies, your repayment strategy must prioritise liquidity to handle the specific maintenance and compliance costs associated with SDA housing.

If your financial profile doesn't fit the standard bank mould, you need a partner who thrives on difficulty. We specialise in securing NDIS property finance and self-employed home loans that other brokers miss. Stop guessing your numbers and start engineering a path to settlement with a team that understands the inner workings of the financial system.

From Calculation to Approval: Engineering Your Optimal Loan Structure with Quantum Brokers

A mortgage repayment calculator is a high-fidelity simulation, but it is not a financial commitment. While the data it produces is vital for your initial strategy, it cannot account for the proprietary credit policies of individual institutions. You have the numbers. Now you need the execution. Navigating the gap between a digital estimate and a funded loan requires a specialist who thrives on technical complexity. This is where the choice between a mortgage broker vs. bank becomes your most decisive tactical move.

We don't just provide a service; we act as your strategic partner in a market that often defaults to "no". Our role is to take the raw data from your mortgage repayment calculator results and stress-test it against real-world lending frameworks. We move with a sense of urgency and efficiency that traditional banks simply cannot match. If you have faced obstacles elsewhere, we specialise in finding the structural solution that unlocks your path to property ownership.

The Tactical Edge: Accessing 40+ Lenders

Your local bank branch has a singular, narrow view of your potential. They are limited to their own products, regardless of whether those products suit your specific financial architecture. We operate with a much broader lens. By accessing a panel of over 40 lenders, we match your data to the lender policy that offers the sharpest tactical edge. We architect solutions for complex income types and unique investment goals that standard retail banks often overlook. This is an elite advocacy service where the lenders pay the commission, not you. You gain a high-performance partner at zero cost to your bottom line.

Unlocking Your Financing: The Next Decisive Step

Education is the foundation, but action secures the asset. Moving from calculation to a home loan pre-approval process is how you signal to the market that you are a serious contender. In the fast-moving 2026 property landscape, where national median dwelling values have climbed to $922,838, hesitation is a liability. You need our 24-hour borrowing power assessment to define your limits before you hit the auction floor.

Prepare for your first strategic briefing by gathering your financial documentation and a clear summary of your investment objectives. We are ready to secure your position. Stop reacting to market fluctuations and start designing your financial victory. Unlock your true purchase power today.

Secure Your Strategic Advantage in the 2026 Market

The 2026 property landscape demands technical precision over guesswork. You've seen how a mortgage repayment calculator serves as the essential blueprint for your cash flow, but the real victory lies in the execution of that design. By mastering repayment velocity through fortnightly schedules and offset accounts, you actively de-risk your debt. Whether you're navigating the high-yield terrain of NDIS property finance or the complex income structures of the self-employed, your loan must be architected for high performance from the outset.

It's time to move from calculation to pre-approval. We provide the tactical edge you need by navigating over 40 Australian lenders to find the specific policy that matches your unique financial data. Our team specialises in NDIS and self-employed finance, ensuring that even the most difficult scenarios result in a successful settlement. Experience the efficiency of our 24-hour borrowing power assessment and take the next decisive step in your property journey. Architect your optimal loan structure with a free Quantum Brokers consultation and secure your future with absolute confidence.

Frequently Asked Questions

How do I calculate my mortgage repayments accurately?

You calculate repayments by inputting the loan principal, current interest rate, and term length into a high-fidelity mortgage repayment calculator. Accuracy depends on using realistic data, such as the 5.94 per cent to 6.44 per cent variable rates seen in early 2026. This provides the structural foundation for your budget before you engage with a specialist to secure a formal pre-approval.

Can I use a mortgage repayment calculator for an NDIS investment property?

You can use a calculator for NDIS properties, but the inputs require a specialist's touch. You must account for the standard 20 per cent deposit requirement and the high rental yields, which often reach 8 to 12 per cent. A standard tool won't model the unique serviceability of SDA housing, so treat the result as a preliminary cash flow estimate only.

How much can I save by switching to fortnightly repayments?

Switching to fortnightly repayments allows you to pay off your debt significantly faster by completing 26 half-payments annually. This effectively adds a 13th monthly payment to your principal reduction each year. Over a standard 30-year term, this simple structural adjustment can shave several years off your mortgage and save you tens of thousands in interest costs.

Is a mortgage repayment calculator reliable for self-employed borrowers?

A mortgage repayment calculator is a reliable diagnostic tool for self-employed borrowers if you use net profit figures from your tax returns. However, it cannot account for the specific "add-backs" that different lenders use to calculate your actual borrowing power. Use the calculator for your internal budgeting, then consult an expert fixer to navigate alternative income verification pathways.

What is the difference between principal and interest repayments?

Principal repayments reduce the actual balance of the money you borrowed, while interest repayments cover the cost of the debt. In the early stages of your loan, your machine is geared toward interest. Strategic borrowers aim to shift this balance toward principal as quickly as possible to build equity and reduce the total lifetime cost of the loan.

Does the calculator account for the First Home Buyers Grant?

Most calculators don't automatically include government incentives like the First Home Owner Grant. You should subtract the grant amount, such as the $10,000 available in metropolitan Melbourne or $15,000 in Queensland, from your total loan requirement before running the numbers. This ensures your repayment estimate reflects the actual debt you intend to secure.

How do interest rate rises affect my monthly repayment figure?

Interest rate rises increase the interest component of your repayment, which can tighten your household cash flow. With the RBA cash rate at 4.35 per cent, even a small shift can have a significant monthly impact. We recommend architecting a "repayment buffer" of 2 to 3 per cent above current market rates to ensure your strategy remains resilient.

What extra costs should I factor in beside the calculated repayment?

You must factor in "hidden" structural costs like council rates, building insurance, and strata fees. If your deposit is under 20 per cent, Lenders Mortgage Insurance (LMI) is a critical variable that increases your total loan amount. Don't build a paper-thin strategy; include at least 1 per cent of the property's value for annual maintenance and compliance.