Why are you still being asked for a 20% deposit when the banking system is engineered to reward your career trajectory? It is a common frustration for healthcare experts; you have the earning potential, but rigid bank policies often ignore your overtime and demand massive upfront capital. You don't have time to chase 40 different lenders while managing a clinical load, and you shouldn't have to. Finding the right home loans for medical professionals is not about asking for a favour. It is about architecting a high-leverage strategy that exploits lender hunger for medical risk.

We're here to help you unlock the tactical advantages of medical-specific lending, from LMI waivers to high-leverage loan structures designed for your specific path. You can secure a high LVR loan without paying a cent in Lenders Mortgage Insurance, potentially saving $20,000 or more on a standard property purchase. This briefing outlines how to optimise your cash flow through strategic structuring and fast-track your approval by ensuring 100% of your shift allowances are recognised. We will show you how to bypass administrative friction and secure the terms your profession has earned.

Key Takeaways

- Learn why lenders categorise healthcare experts as a high-performance tier and how this translates into aggressive interest rates.

- Discover how to bypass Lenders Mortgage Insurance entirely while securing up to 95% or 100% of your property value.

- Master the art of income architecting to ensure banks recognise 100% of your overtime and shift allowances when assessing home loans for medical professionals.

- Identify the specific criteria that allow allied health experts and nurses to unlock high-leverage financing typically reserved for surgeons.

- Understand the tactical advantage of using a specialist broker to access 40+ lenders rather than settling for a single bank's generic medical package.

The Medical Advantage: Why Lenders Compete for Your Business

Banks don't just like doctors. They crave the risk profile you represent. In the high-stakes world of Australian finance, medical practitioners are categorised as a high-performance tier. This status isn't about prestige; it's about the cold, hard data. Historically, medical professionals have some of the lowest default rates in the country. Even during economic shifts, your income remains remarkably recession-proof. Lenders recognise this stability and are willing to bend their own internal rules to secure your business. This creates a unique opportunity to access mortgage loan basics while bypassing the restrictive barriers that hold standard borrowers back.

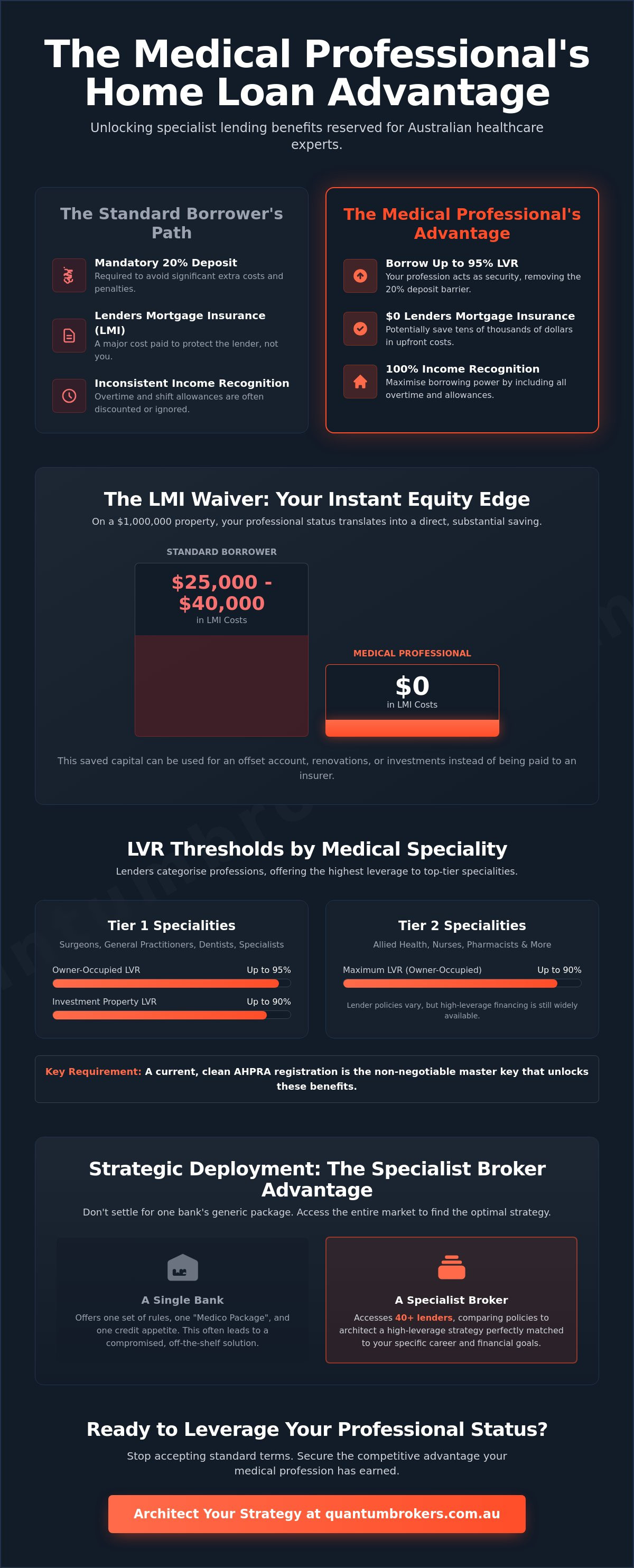

When we talk about home loans for medical professionals, we aren't discussing standard products found on a bank's public website. We are talking about policy exceptions. These are internal banking frameworks that allow for higher leverage and lower costs based purely on your AHPRA registration. While standard borrowers are forced to provide a 20% deposit to avoid penalising fees, your professional status serves as a master key to the credit vault.

This specialist approach is a hallmark of medical finance worldwide; for example, practitioners in the UK often consult with experts like Mortgages for Doctors to navigate their own specific professional lending frameworks.

The LMI Waiver: Your Instant Equity Edge

Lenders Mortgage Insurance (LMI) is a one-off premium paid by the borrower to protect the lender, typically required whenever the deposit is less than 20%. For most Australians, it's a massive sunk cost that adds nothing to the property's value. However, a surgeon or GP can often secure a 90% or even 95% LVR without paying a cent in LMI. On a $1 million property purchase, this tactical win translates to an instant saving of approximately $25,000 to $40,000. That is capital you can keep in your offset account or use for an immediate renovation rather than handing it over to an insurance company.

Lender Appetites in 2026

As of June 2026, major Australian banks have doubled down on their dedicated "Medico" desks. They aren't just competing on interest rates, which currently hover between 5.69% and 6.39% p.a. for variable products. They are competing on policy flexibility. While the "Big Four" offer reliability, specialist medical lenders often provide more aggressive structures for private practice owners or those with complex trust setups. Strategic selection is vital when comparing home loans for medical professionals because no two lenders assess medical income the same way. Success requires more than just applying at your local branch; it demands a tactical choice from across 40+ lenders to find the one whose current appetite matches your specific career trajectory.

Decoding the Specialist LVR: Financing Up to 95% Without LMI

Standard lending is designed for the average employee. It assumes that if you lack a 20% deposit, you're a risk. For healthcare experts, this assumption is fundamentally flawed. High leverage does not mean high risk when your career trajectory is practically guaranteed. This is why home loans for medical professionals allow you to borrow up to 95% of a property's value without the dead weight of Lenders Mortgage Insurance. You aren't being penalised for a smaller deposit; you're being rewarded for your stability.

While standard government-backed loan programs might offer low-deposit options to the general public, they usually come with strict income caps or higher interest rates. In contrast, your medical status unlocks high-leverage financing at the same aggressive rates usually reserved for borrowers with massive equity. The gatekeeper to these benefits is your AHPRA registration. Current, clean registration is the non-negotiable requirement that triggers these policy exceptions across the banking sector.

LVR Thresholds by Speciality

Lending appetite is not uniform across the hospital floor. Surgeons, GPs, and Dentists sit at the peak of the hierarchy, frequently securing 95% LVR for owner-occupied residences and up to 90% for investment properties. Other specialities, often referred to as Tier 2 in lender internal guidelines, might see a cap at 90% LVR depending on the bank's specific appetite for that quarter. If you're buying with a non-medical partner, the LMI waiver still applies. As long as the medical professional is a co-borrower and meets the criteria, the entire loan is structured under the specialist framework.

The 100% Finance Myth vs. Reality

You may have heard whispers of 100% finance. While rare, it is technically achievable for specific cohorts like interns or registrars with high growth potential, often facilitated through specialist banking packages. These packages can be powerful, but they often carry higher annual fees or restrictive terms that limit your future flexibility. It's about weighing the immediate LMI savings against the long-term cost of the "package."

Understanding The High-Performance Guide to Australian Home Loans provides the broader context you need to see how these LVRs stack up against standard market benchmarks. If you want to see which threshold your specific speciality triggers, it's time to consult with a strategic architect who can map out your options across the entire market rather than a single bank's limited offering.

Income Architecting: Navigating Overtime, Shift Allowances, and Private Practice

Standard bank assessments are a bottleneck for high-earning clinicians. Most lenders look at a complex medical payslip and see volatility. They see shift allowances and overtime as "variable" and immediately discount them by 20% or more. This is an amateur mistake that ignores the reality of the healthcare sector. When architecting home loans for medical professionals, we ensure lenders recognise the structural stability of your income. We target institutions that accept 100% of your overtime and allowances, which can add hundreds of thousands to your borrowing capacity without requiring a change in your base salary.

For registrars transitioning to consultant roles, the "Future Income" policy is a critical tactical lever. If you've signed a contract for a specialist position, specific lenders will assess your application based on that future salary up to three months before you even start the role. This allows you to bypass the "wait and see" approach of traditional banking and secure your property while you're still in training. It is a high-performance move that standard lenders rarely offer. You can find more global context on these structures in this Ultimate Guide to Physician Mortgages, though the Australian market requires a more localised, technical approach to succeed.

The Overtime Advantage

Specialist lenders view medical overtime as a structural certainty of the profession rather than a discretionary bonus, allowing for a more aggressive assessment of your true earning power. To bypass the standard "shading" of your income, we present two years of PAYG Income Statements to demonstrate a consistent pattern of hours. This evidence forces the lender to treat your variable shift work as a fixed, reliable income stream; ensuring your loan is assessed on what you actually earn, not a conservative bank estimate.

Private Practice and Self-Employed Medicos

Operating through a private practice or a Service Trust introduces layers of complexity that often baffle standard mortgage brokers. Your taxable income might be intentionally minimised for tax efficiency, but this shouldn't cripple your borrowing power. We use "add-backs", such as depreciation on medical equipment, non-recurring expenses, and superannuation contributions, to reconstruct your true financial strength. Even if you've been in private practice for less than two years, we can often secure approval by leveraging your previous hospital experience as a continuous career path. For a technical breakdown of how we handle these business structures, see our dedicated guide to Self-Employed Home Loans. We don't just fill out forms; we architect a case that proves your practice is a high-performance asset.

Beyond the Stethoscope: Home Loan Perks for Allied Health and Nursing

The banking industry often suffers from tunnel vision. Most lenders reserve their best "medico" policies for surgeons and GPs, completely ignoring the high-performance allied health and nursing sectors. This is a strategic failure. If you're an optometrist, pharmacist, or clinical psychologist, you belong to a "hidden" tier of professionals who qualify for significant lending advantages. When architecting home loans for medical professionals, we look beyond the stethoscope to secure the same LMI waivers and high-leverage structures for the broader healthcare workforce.

Eligibility for these perks isn't just about your job title; it's about your professional registration and, frequently, your income trajectory. While doctors often get a "no-questions-asked" pass, allied health professionals usually need to meet specific income thresholds to trigger an LMI waiver. We specialise in identifying the lenders who have the highest appetite for your specific speciality, ensuring you don't waste time with institutions that have rigid, outdated exclusion lists. Success in this space requires a broker who knows which lenders treat your AHPRA registration as a high-value asset rather than just another piece of paperwork.

Allied Health Eligibility List

Lender appetite for allied health varies wildly across the market. While some banks only want to talk to dentists, others have designed blueprints specifically for:

- Physiotherapists and Occupational Therapists

- Chiropractors and Osteopaths

- Pharmacists and Optometrists

- Psychologists and Radiographers

- Podiatrists and Speech Pathologists

To unlock an LMI waiver, many lenders require a minimum annual income of $90,000 to $150,000 depending on the specific role and lender policy. If you fall below this, we don't just accept a "no." We pivot to lenders who prioritise professional body membership or AHPRA registration over raw salary figures to secure your approval. It's about matching your professional profile to the right credit policy.

Nursing and Midwifery Strategies

Nurses and midwives are the backbone of the system, yet standard banks often struggle to calculate their true borrowing power. They see complex shift-work patterns and salary packaging as administrative friction. We turn this into a tactical advantage. By correctly architecting your salary packaging and shift allowances, we can often push your serviceability higher than a standard PAYG assessment would allow. For most nurses, a 90% LVR is the strategic "sweet spot." It allows for a manageable deposit while still qualifying for LMI waivers at specific institutions, provided you meet the $90,000 income threshold. If you're ready to stop fighting with generic bank staff, contact our strategic architects to design a loan that actually reflects your career value.

Strategic Deployment: Securing Your Medical Home Loan with Quantum

Time is your most depleted resource. Between clinical rotations, private practice management, and continuing education, you don't have the luxury of navigating the slow, grinding bureaucracy of a retail bank. Standard lenders often treat home loans for medical professionals as a generic checkbox exercise. They offer a "one-size-fits-all" medical package that might look attractive on the surface but often contains hidden limitations or uncompetitive rates. We don't just apply for loans. We architect a tactical deployment across the entire market to ensure your finance matches your professional status.

Precision matters in the theatre, and it matters in your property portfolio. Bureaucracy kills deals, especially in a fast-moving market where a delayed approval means a lost opportunity. Our methodology is built on speed and technical mastery. We understand the inner workings of the financial system better than the institutions themselves. By acting as your Strategic Architect, we remove the administrative friction and force lenders to compete for your business on your terms.

The Quantum Advantage: 40+ Lenders, One Tactical Lead

Relying on a single bank's medical package is a high-risk strategy. If their internal policy shifts or their appetite for medical risk changes, your application hits a dead end. We eliminate this single point of failure by stress-testing your application across 40+ lenders simultaneously. This Zero-Error blueprint identifies the institutions with the most aggressive LMI waivers and the highest recognition of your specific income streams. We don't hope for an approval; we engineer a victory. Unlock your borrowing power with our 24-hour calculator and see how we can fast-track your next acquisition.

NDIS Investment: The Ultimate Medical Synergy

Your expertise in healthcare gives you a unique perspective on the Australian property market. While standard investors struggle to understand the complexities of Specialist Disability Accommodation (SDA), you already recognise the clinical necessity and the long-term demand. Medical professionals are uniquely positioned to capitalise on NDIS housing, turning their high-leverage home loans for medical professionals into a springboard for high-yield investment. We specialise in helping medicos pivot from owner-occupied property into the lucrative SDA space. To understand how to structure these complex builds, explore our insights as an NDIS Property Finance Specialist Australia. It is about using your professional status to build a recession-proof wealth engine.

Deploy Your Professional Advantage

Stop accepting the "no" from banks that don't understand your income. You've earned the right to high-leverage financing through years of clinical dedication. By architecting a strategy that bypasses LMI and recognises 100% of your overtime, you secure an immediate equity edge. Whether you're a surgeon or an allied health specialist, the market is ready to compete for your business. It is time to stop playing by standard rules and start exploiting the tactical advantages your profession provides.

Securing the best home loans for medical professionals isn't about luck; it's about technical mastery. We provide access to 40+ Australian lenders and specialise in securing 90-100% LVR structures that retail branches simply cannot match. From free pre-approval to complex strategic loan structuring, we handle the administrative friction so you can focus on your patients. Don't settle for a generic banking package that limits your wealth potential or forces a massive deposit you don't need to pay.

Architect your medical home loan strategy with Quantum Brokers. Your career is recession-proof; your property finance should be too.

Frequently Asked Questions

Do I need to be a permanent resident to get a medical home loan?

No, you don't necessarily need permanent residency to access these benefits. Many Australian lenders offer specialised policies to temporary residents on eligible visas, such as the 482 or 186, provided you hold current AHPRA registration. While foreign citizen stamp duty surcharges may apply depending on your state, your professional status allows us to negotiate terms that standard visa holders cannot access.

Can I get an LMI waiver if I am a medical intern or registrar?

Yes, interns and registrars are eligible for LMI waivers from day one of their internship. Lenders view your career path as a guaranteed trajectory toward high earnings, making you a low-risk prospect even at the start of your journey. We often secure approvals using only a signed employment contract, allowing you to purchase property before you even receive your first payslip of the new clinical year.

Does HECS/HELP debt significantly impact my borrowing capacity as a doctor?

HECS debt does reduce your borrowing power because it lowers your net take-home pay, but it's rarely a barrier to approval. Because your income potential is significantly higher than the Australian average, the impact of a HECS balance is often secondary to your overall serviceability. We architect your application to emphasise your future earning growth, which helps satisfy lender stress tests despite existing student debt.

Which medical specialities qualify for the 95% LVR home loan?

GPs, Surgeons, Dentists, and Veterinarians almost always qualify for 95% LVR home loans for medical professionals without paying LMI. This list often extends to Optometrists and Pharmacists at specific institutions. We verify your AHPRA category against the internal "white-lists" of 40+ lenders to ensure we deploy your application where it will receive the highest possible leverage.

Can I use my medical home loan benefits for an investment property?

Yes, you can apply your professional benefits to investment acquisitions, though the leverage limits are usually tighter than owner-occupied loans. Most lenders cap investment LVRs at 90% without LMI. This is still a massive advantage over standard investors who are typically forced to provide a 20% deposit or pay thousands in insurance premiums to reach the same level of debt.

What documents do I need to prove my overtime income?

You generally need your two most recent payslips and your most recent PAYG Income Statement to prove overtime. We use these documents to establish a clear pattern of consistency. By demonstrating that your overtime is a structural part of your role, we force the bank to recognise 100% of those earnings rather than discounting them by the standard 20% margin.

Are interest rates higher for medical home loans with low deposits?

No, interest rates for home loans for medical professionals are typically the same as those offered to borrowers with a 20% deposit. You don't suffer the "low equity" pricing penalties that standard borrowers face. You get the best of both worlds; the high leverage of a 5% deposit combined with the aggressive, discounted interest rates usually reserved for high-equity clients.

How long does the approval process take for a medical professional?

Approval typically takes between 3 and 5 business days once your documentation blueprint is complete. Because we submit directly to dedicated medical lending desks, your application bypasses the standard retail credit queues. This priority channel ensures a faster turnaround and a more sophisticated assessment from credit officers who actually understand the complexities of medical payslips and private practice structures.